In the rarefied world of Swiss horology where precision is not merely a mechanical virtue but a philosophical creed to be accused of inaccuracy is no small affront. Yet that is precisely the charge levelled by The Swatch Group against Morgan Stanley Investment Management over its Ninth Annual Swiss Watcher report dated 18 February 2026. The response came not as a murmured objection but as a formal open letter meticulous pointed and devastating in tone.

At the heart of the dispute lies a paradox. Morgan Stanley publicly affirms in its Code of Ethics that it must deal fairly and act in the best interests of its clients at all times and on its homepage proudly champions its reputation for timely in depth analysis. Swatch Group contends that the report in question does precisely the opposite offering speculative estimations dressed in the raiment of empirical certainty.

The Illusion of Data

The report cites five principal data sources public company disclosures CEO statements direct brand discussions data from the Fédération de l’Industrie Horlogère Suisse and broader industry dialogue. On the surface this appears robust. In practice Swatch Group argues two of these listed company reports and FHS export data do not provide brand level detail at all. Their inclusion the Group suggests serves to create an illusion of rigour rather than its substance.

The remaining sources CEO remarks and informal industry conversations are by their very nature anecdotal and unverified. Luxury analyst commentary cited in Le Temps wryly observed that brand owners delight in everything an acknowledgment that executive optimism is hardly a statistically reliable metric. Yet from this fragile scaffolding the report extrapolates precise turnover figures unit sales market shares and average retail prices down to decimal points.

Precision Swatch argues becomes a theatrical device. A claim such as a 16.1 percent market share in 2025 implies scientific exactitude. In reality it is a point estimate resting on unverifiable foundations. Reputable research the Group insists would employ ranges not singular figures when dealing with such uncertainty.

When Estimates Become Errors

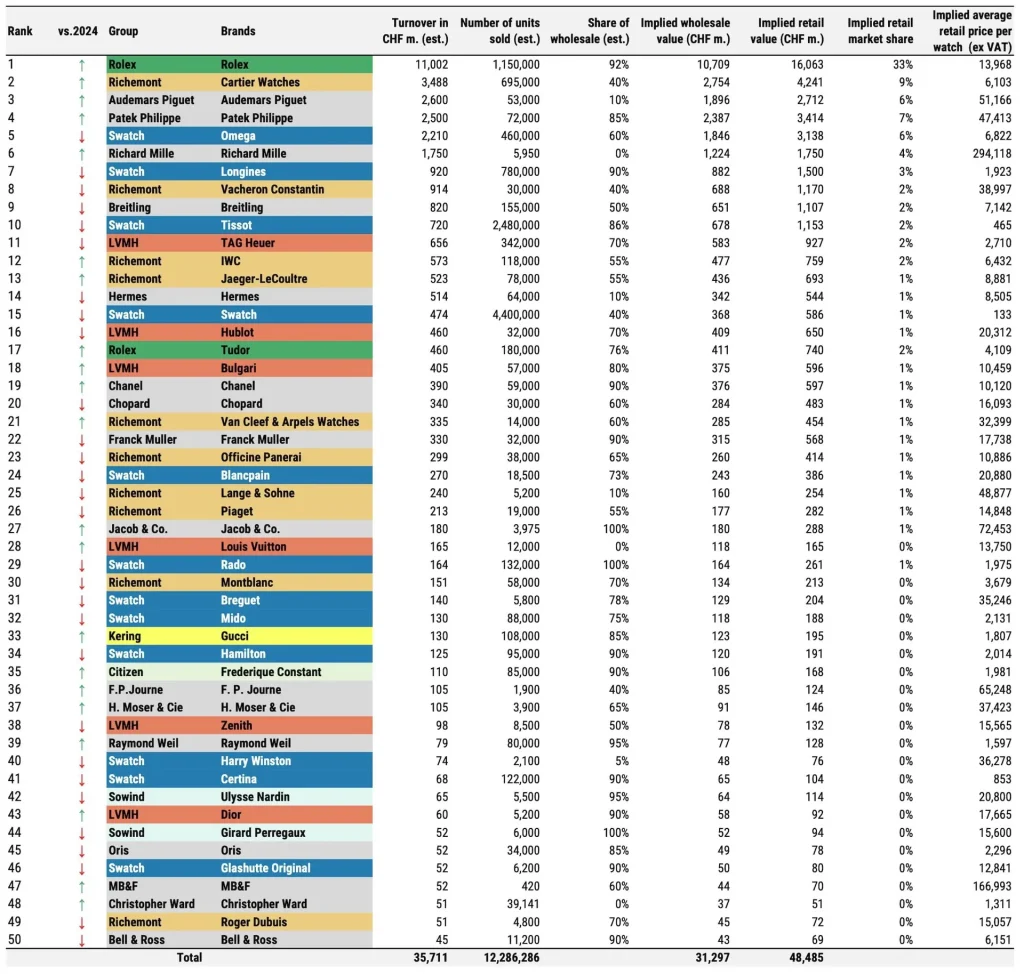

The consequences of this methodological looseness are stark. Swatch Group claims that across its brands turnover deviations average 24 percent with discrepancies ranging from minus 53 percent to plus 46 percent. Unit sales even more dramatically show an average variance of 35 percent stretching to an astonishing 198 percent in the case of Hamilton where actual unit sales are said to be triple the report estimate.

Retail share assumptions fare no better. For Breguet the report assumes 22 percent retail share while the actual figure according to the Group is 54 percent. For Longines the estimate stands at 10 percent versus an actual 24 percent. For Swatch the report posits 60 percent while the Group claims 86 percent.

Retail prices calculated from these layered assumptions compound the distortion. The report suggests an average retail price of CHF 2131 for Mido while Swatch states the real figure is CHF 969. For Hamilton CHF 2014 is asserted versus an actual CHF 741.

Perhaps most illustrative is the case of Breguet. Earlier reports implied an average retail price of CHF 15000. Upon being informed that this was inaccurate the figure was doubled the following year yet turnover estimates remained unchanged. Unit sales were simply halved to preserve narrative symmetry. To Swatch this is not analysis it is retroactive arithmetic.

Also Read: Tissot MotoGP Collection: Official Racing Timepiece For Speed Enthusiasts

Rankings Built on Sand

From these contested numbers emerge industry rankings bold headline ready and Swatch argues fundamentally unreliable. The report claims that Omega fell to fifth place overtaken by Audemars Piguet and Patek Philippe. With average deviations of 24 percent however Omega could plausibly rank anywhere between second and sixth. The certainty of ordinal position dissolves under statistical scrutiny.

Reputational Harm

More troubling than methodological flaws are what Swatch describes as defamatory and potentially damaging statements. The report alleges that several Swatch brands suffered turnover contractions exceeding 15 percent in 2025 and that Longines became loss making calling it the Group main problem child.

Swatch counters that Tissot actually grew by 3 percent not declined by 5 percent and that Longines posted a 16.6 percent profit margin on net sales. Such assertions the Group warns risk undermining retailer confidence and consumer trust. In luxury perception is capital.

Conflicts and Transparency

While Morgan Stanley includes a disclaimer acknowledging potential conflicts of interest the report author LuxeConsult offers no such disclosure. Given that much of the data purportedly arises from direct brand dialogue Swatch questions the impartiality of the exercise.

Also Read: Rattrapante Chronograph Guide: Working, History And The 5 Best Split-Seconds Watches To Buy

The Larger Question

Ultimately this dispute transcends brand pride. It interrogates the very nature of financial research in industries where hard data is scarce and private companies abound. Swatch Group objection is less a defensive reflex and more a philosophical stance that speculation however elegantly presented must not masquerade as fact. In horology tolerances are measured in microns. Swatch Group appears to be reminding the financial world that intellectual precision demands no less.